Bioverge Biotech Intelligence – Q3'25 Edition

Exclusive Insights for Biotech Investors, Issue: Q3 2025

Disclaimer: This content is provided for educational and informational purposes only and does not constitute investment advice or a recommendation to buy or sell any securities. It was prepared with the assistance of AI and may contain inaccuracies or unintended errors that were not identified during the final review and editing process. Bioverge, or individuals affiliated with Bioverge, may hold positions in the securities mentioned. All referenced positions and model scenarios and portfolios should be considered illustrative and hypothetical. Always conduct your own due diligence before making investment decisions.

Introduction

Welcome to the second edition of the Bioverge Biotech Intelligence Newsletter. After debuting the inaugural Q2’25 edition to our LPs in April, we’re now making it available to a broader audience. All portfolio allocations reflect positions initially taken in early Q2 2025, giving you transparency into our conviction bets ahead of market catalysts. We’ve since adjusted the portfolio based on new data and market fluctuations, as detailed below.

We’ll publish a comprehensive issue at the beginning of each quarter, with select interim updates as news, performance, or portfolio shifts warrant.

1. Market Pulse: Biotech Performance & Sector Trends

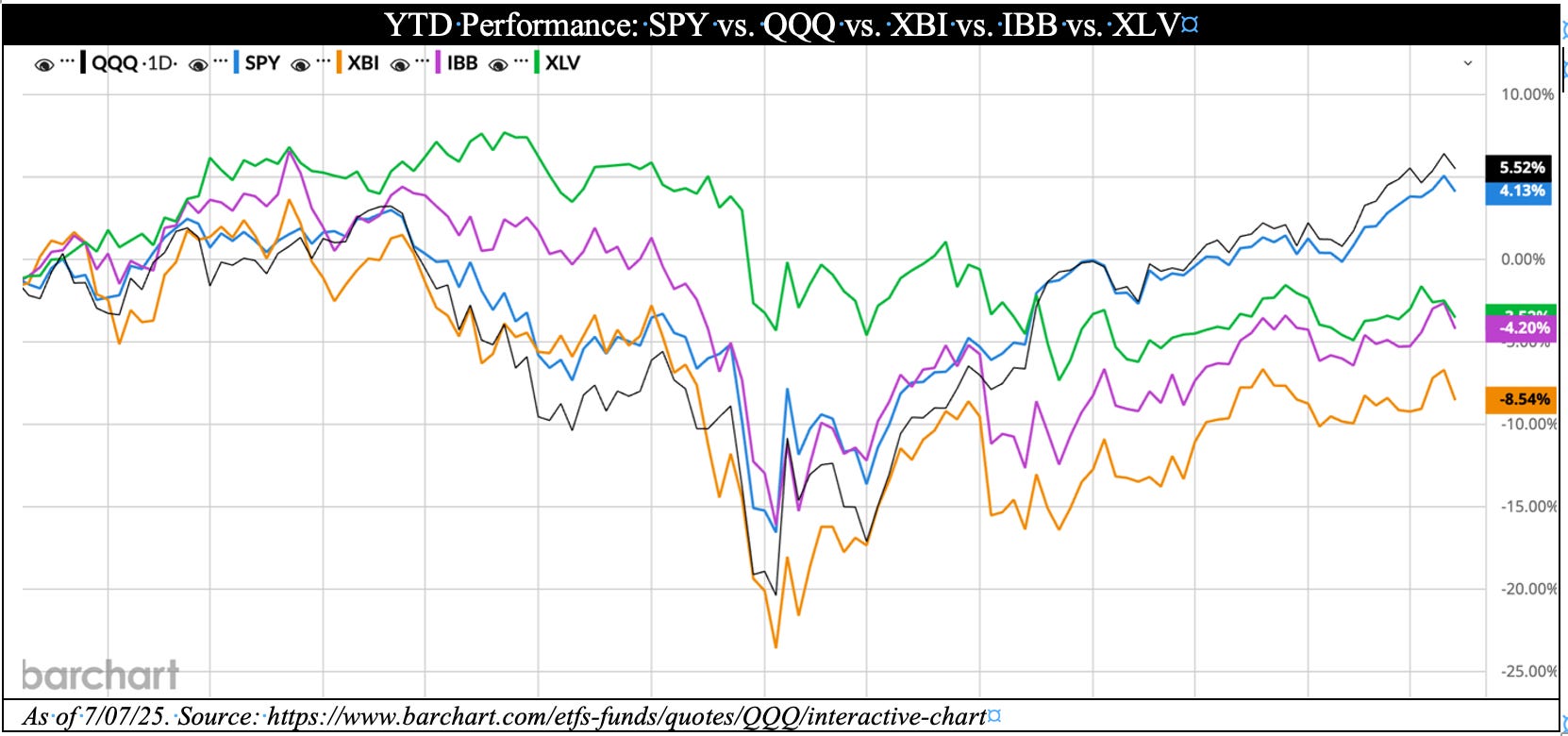

While the broader market has posted solid gains this year—driven by continued strength in tech and AI—the biotech sector has lagged meaningfully behind. While the S&P 500 is up 4.1% YTD, the IBB and XBI are down 4.2% and 8.5%, respectively. Persistent regulatory uncertainty, pricing pressures, and capital constraints continue to weigh on sentiment, despite accelerating innovation across areas like cell therapy and gene editing.

We believe this dislocation presents opportunities for long-term investors with a disciplined approach.

YTD Performance: SPY vs. QQQ vs. XBI vs. IBB vs. XLV

3-Year Performance: SPY vs. QQQ vs. XBI vs. IBB vs. XLV

🧬 Q3 2025 Biotech M&A: Key Developments Driving the Sector

Biotech M&A activity has been robust in 2025, with big pharma deploying capital to acquire clinical and platform-stage assets that fill strategic pipeline gaps. Below are the key developments this quarter:

🔹 Lilly acquires Verve Therapeutics. In a bold bet on gene editing, Eli Lilly announced the acquisition of Verve Therapeutics for ~$2.9B, gaining access to Verve’s in vivo base editing platform for cardiovascular disease. This deal reflects renewed confidence in next-generation gene editing and adds to Lilly’s growing portfolio in cardiometabolic disease following the success of tirzepatide.

Note: We initially considered including VERV in our portfolio, however, decided to include a position in Beam instead….see our post-mortem below! We did, however, start building a position in Prime Medicine before the recent runup and have seen a quick 100%+ appreciation since our purchase, details below!

🔹 BioNTech to acquire CureVac. BioNTech is acquiring CureVac in an all-stock deal (~$1.25B), consolidating mRNA oncology capabilities and accelerating development of personalized cancer vaccines—highlighting continued interest in mRNA beyond COVID-19.

🔹 Sanofi buys Blueprint Medicines. Sanofi is purchasing Blueprint for up to $9.5B, driven by strong performance of Ayvakit in systemic mastocytosis. This marks one of the largest rare disease acquisitions of the year and signals big pharma’s appetite for de-risked commercial-stage assets.

Note: This has put other rare disease companies on the M&A target list and we’re closely watching Ultragenyx and BridgeBio (we’ve been following BBIO for a long time now, and that’s another near miss in our portfolio).

🔹 GSK acquires Verona Pharma. GSK is acquiring Verona Pharma for ~$1.1B in a bid to expand its respiratory portfolio with ensifentrine, a first-in-class dual PDE3/4 inhibitor for COPD. The deal gives GSK access to a late-stage, inhaled therapy with positive Phase 3 data and commercial launch readiness, reinforcing its strategic focus on specialty-driven assets with near-term revenue potential.

🔹 Merck KGaA acquires SpringWorks Therapeutics. Merck KGaA is acquiring SpringWorks for ~$3.9B, bolstering its oncology portfolio with a late-stage NTRK inhibitor and continuing its strategic focus on targeted cancer therapies.

Key Takeaways:

Cardiometabolic and gene editing platforms are heating up, as seen in Lilly–Verve.

Late-stage oncology and rare disease assets remain top M&A targets, with multiple multi-billion-dollar takeouts in these areas.

mRNA innovation continues to attract long-term capital, particularly in oncology.

Mid-cap buyers are selectively acquiring undervalued clinical-stage players, signaling opportunities even in a depressed market.

2. Portfolio Updates & Performance

Executive Summary

We constructed a diversified biotech portfolio that maximizes risk-adjusted returns over a 5-year horizon (see our inarguable Q2’25 newsletter for a detailed Monte Carlo analysis and portfolio construction). This strategy combines public market exposure with a curated venture sleeve to harness both compounders and asymmetric return opportunities, while minimizing downside risk.

After several rounds of optimization, we arrived at the following diversification across Risk tiers and allocations:

Core (60%): Lower-volatility, large-cap biopharma for stability

Growth (20%): Mid-cap/late-stage clinical biotechs with upside

Moonshots (10%): Small-cap, preclinical/early-stage innovators

Venture Sleeve (10%): Access to illiquid opportunities with exponential return potential

The portfolio blends our scientific insight with quantitative rigor to deliver a powerful risk-adjusted profile over a 5-year horizon.

Keep reading with a 7-day free trial

Subscribe to Bioverge’s Substack to keep reading this post and get 7 days of free access to the full post archives.